Conclusion

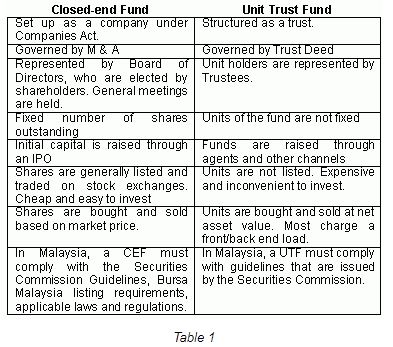

In the last 6 parts of this special series, i Capital provided a detailed analysis of closed-end funds (CEF) and unit trust funds (UTF), elucidating what they are, how they work, their regulatory framework, how they are marketed, their past performance, and their unique characteristics. This week, we will conclude this series on collective investments schemes. Common examples of collective investment schemes (CIS) would be unit trust funds (UTF) and closed-end funds (CEF). The ordinary Malaysian investor would have plenty of experience with UTF but few would be familiar with CEF. Table 1 summarises some of the salient characteristics of CEFs versus UTFs.

A CIS is a scheme where a group of investors with the same or similar investment objectives pool their money together and invest. Usually these investors do not have the skills, time, funds or resources to invest on their own. As such, they pool their funds and pass it to professionals to manage it for them. A CEF is similar to a UTF in that they are both professionally managed CIS, but there are major differences in the way the 2 vehicles are structured and operates. It is due to these differences that CEFs reward investors with very important benefits that UTFs just simply cannot as explained below.

[a]. Closed versus open

CEFs have a fixed number of shares outstanding. In contrast to UTFs, the amount of funds available for investment remains stable for CEFs. This is the reason why they are called closed-end. In the case of UTF, the number of units is flexible and is affected by inflows of new funds and redemption of existing units. This is the reason why UTFs are also called open-end funds. The fact that is one open-ended while the other is close-ended has major implications. Why?

[b]. Who really is the fund manager?

CEFs have a fixed number of shares outstanding and the amount of funds available for investment remains stable for CEFs. In the case of UTF, the number of units changes constantly. This is a very important distinction given that stock markets are driven by cycles of fear and greed.

Fund managers of CEFs need not have to worry about inflows and outflows of funds, whereas fund managers of UTFs have to constantly worry about having enough cash to meet redemption requests or to invest the new funds flowing in.

During the peak of the market or periods of greed, UTFs experience heavy inflows of funds. Fund managers of UTF have no choice but to invest at the peak even though valuations are expensive. Conversely, during periods of fear or panic, UTFs experience heavy outflows of funds or redemptions. Fund managers of UTFs are then forced to sell their investments to meet redemption requests, even if it requires them to sell at cheap prices. This essentially means that the real fund manager in the case of UTFs is actually the individual unit trust holders and not the appointed fund manager. UTF fund managers have to act and decide according to the greed and fears of its individual unit holders. In stark contrast, for a CEF, the shareholder?s buying and selling activities have no impact on the funds available for investing. The fund manager’s investment decisions are totally separated from what the shareholders decide to do.

[c]. Better investment opportunities

Given the fact that CEFs do not experience inflows and outflows of funds, their fund managers have a broader range of investment choices and greater flexibility in deciding where and how to invest. This allows them the following advantages :

- • Invest with a long-term strategy;

- • Invest in undervalued but relatively ‘illiquid’ securities;

- • Invest in smaller capitalised securities and

- • CEFs can be more focused when investing.

As CEFs can be more focused when investing, CEFs offer potentially higher returns.

[d]. Lower expenses, better returns

As we all know, expenses are bad for returns. Fortunately, CEFs have lower expenses than UTFs. Why?

As CEFs have a fixed number of shares outstanding, there is no need for continuous and expensive marketing and distribution expenses. UTFs, on the other hand, have an extensive and expensive marketing and distribution network and the costs are borne by the individual unit trust holders through the loading fees, which can range from 2 to 7% of net asset value (NAV).

Since CEFs do not experience constant inflows or outflows of funds, CEFs do not have to buy and sell their investments frequently. With a lower portfolio turnover, this means that CEFs can have much lower stock broking commissions than UTFs.

[e]. Less reinvestment problems

Since CEFs have a fixed number of shares outstanding, they do not experience constant inflows or outflows of funds. Therefore, CEFs have less trading activities. With less buying and selling to do, CEFs would have less reinvestment decisions to make. Why is this important?

The more reinvestment decisions there are, the higher the risks of making the wrong decisions and thus the higher the chances that the performance of a fund would be inferior. As a result, the chances of success for CEFs are much higher.

[f]. Premium/Discount

Like all other listed companies, the market prices of CEFs need not equal their NAVs. Again, like the share price of any listed company, a CEF may trade at a premium or discount to its NAV. For CEFs, the discount/premium is a feature that provides investors with the potential for additional returns. When the CEF?s premium widens or its discount narrows, the return of the CEF, based on its share price, will be greater than the NAV return. This premium/discount feature cannot be found in UTFs.

[g]. Superior Performance

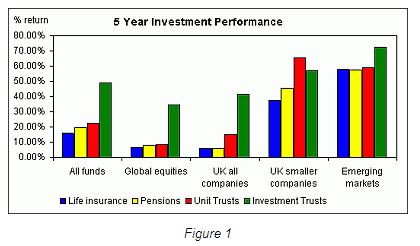

While the only closed-end fund in Malaysia has performed poorly, CEFs have proven to be a superior investment vehicle overseas. Its prowess over other investment vehicles is clearly demonstrated in Figure 1. Looking at the 5-year performance comparison of various investment vehicles in a sophisticated market like the UK, CEFs (known as investment trust in the UK) outperformed life insurance, pensions and unit trusts in all fund classes, except for UK Smaller Companies.

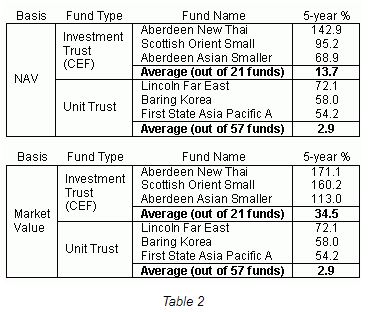

The superior investment performance of CEF?s is again seen by comparing the top 3 performing CEFs with the top 3 performing UTFs in a matured market like the UK. Table 2 shows the Far East, Ex-Japan category. Table 2 has two segments – the upper segment is a comparison based on NAV and the lower segment is comparing performance of CEF and UTF based on share price or market value. Since UTFs are not listed, note that the performance of UTFs in the upper and lower segment is the same which is not the case for CEFs.

- • Based on NAV return, the top 3 performing CEFs outperformed the top 3 performing UTFs;

- • Based on market value, the top 3 performing CEFs far outperformed the top 3 performing UTFs;

- • The average return for CEFs far exceeded the average return for UTFs,based on NAV;

- • The average return for CEFs far exceeded the average return for UTFs, based on market value and;

- • With the help of the narrowing of discounts or widening of premiums, the market value returns were much higher than the NAV returns for CEFs.

[h]. What drives performance?

Having established CEFs as a superior investment vehicle, how does one then determine which CEFs would offer superior returns? Looking at Table 2, we see a huge difference between the returns generated from the top performing CEF and the average performer, on both NAV and market value return. A critical question to ask then is what drives performance?

Fund managerCeteris paribus, it is the skill and ability of the fund manager that differentiates a superior fund from an average fund. If you have a lousy fund manager, then the CEF will not perform. But if the CEF has a top performing fund manager, the CEF will produce top class performance. Furthermore, the track record of any CEF would essentially belong to a specific fund manager. If the fund manager leaves, then the track record of the CEF actually follows the fund manager. It is therefore imperative that an investor knows whom the CEF?s track record belongs to before investing.

Track recordAn immediate filter that is commonly used to identify a top performing fund manager is his/her track record. Investors always invest based on past performances, but as we all know past performance is not a guarantee of future performance. What is important to investors is how the fund manager can ensure future investment success and how first-rate performances can be repeated. In essence, fund managers can achieve these goals only by providing a total commitment and having a sound and rational investment framework.

Total commitmentBut how do you identify a fund manager with total commitment? For a start, an independent structure is very important as this prevents conflicts of interest. Many fund management companies are usually part of large financial groups who may have, amongst others, a stock broking arm, a unit trust management company and a merchant bank. In such groupings, there are many interests and sources of income to look after, and it is unclear where the loyalties lie. In contrast, for an independent fund manager with only one source of income, the focus and loyalty to its clients is very clear.

Sound Investment framework and philosophyOther than a total commitment, an independent structure and integrity, the fund manager must also have a sound and rational investing framework. A sound investment framework with a clearly defined investment philosophy will guide fund managers in their investment decision making process so that decisions are consistently based on a set of carefully thought out criteria and not emotions or rumours or tips or hearsay. An important reason why many fund managers do not perform well is because they lack an intellectually sound investment framework.

In the fund management industry, the size of the fund managed and the set up tell nothing about the investment performance. It is actually the grey matter that matters. It is the investing philosophy and the organisational structure that truly differentiates a good fund manager from a lousy fund manager.

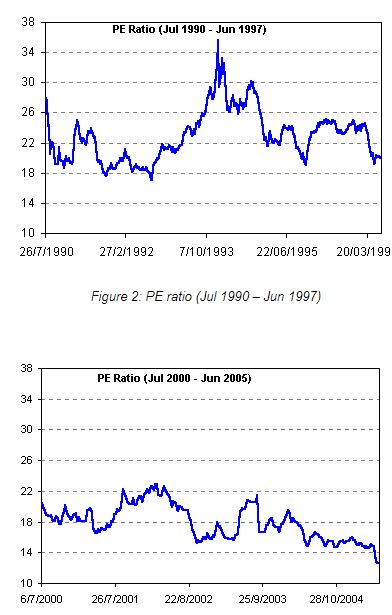

Stock market valuationBut besides the quality of the fund manager, a complementary factor that has a bearing on the performance of a CEF is the timing of its launch. From the perspective of the fund manager, the best time to launch a CEF or any other collective investment scheme is in a hot market. During bull markets, it is much easier for fund managers to sell their funds. However, from the shareholder?s point of view, the best time to launch a CEF is when the market is undervalued. The KLSE is currently trading at a PE of about 13 times, the lowest in the last 15 years as shown in Figure 2 and 3. The time is ideal for the launch of a CEF in Malaysia.